Antiques Donation Appraisal Guide How Documentation Should Be Prepared: appraisal and value basics

Antiques Donation Appraisal Guide How Documentation Should Be Prepared research should start with identification, condition, provenance, and recent comparable sales. Use this guide to compare the signals that matter before paying for a formal appraisal or deciding whether to sell.

Donating antiques to a qualified charity can be one of the most tax-efficient ways to pass along a collection you no longer wish to maintain. But the IRS treats donated antiques differently than cash gifts — and the burden of proof sits squarely on the donor.

A well-documented appraisal file is your primary shield. It includes photographs, provenance records, purchase receipts, restoration logs, and a formal qualified appraisal signed by a credentialed professional. Without that file, a charitable deduction for antiques is vulnerable to disallowance.

This guide walks through every document you should gather, how to photograph your pieces, what makes an appraisal "qualified" under IRS rules, and the Form 8283 steps that protect your deduction. Whether you are donating a single Chippendale chair or an entire estate collection, the same documentation discipline applies.

When You Need a Qualified Appraisal for Donated Antiques

The IRS draws a sharp line at $5,000. If the fair market value of a donated antique — or a group of similar items donated to the same organization in the same year — reaches or exceeds that threshold, you must attach a qualified appraisal to your return using Form 8283, Noncash Charitable Contributions.

Key thresholds to know:

- Under $250: A contemporaneous written acknowledgment from the charity is recommended but not always required. Keep a receipt or bank record.

- $250–$4,999: You must obtain a contemporaneous written acknowledgment from the charity describing the items (but not valuing them). Your own records — photos, receipts, provenance notes — should support the claimed deduction.

- $5,000 and above: A qualified appraisal is mandatory. The appraiser must sign Part III of Form 8283, and the receiving charity must countersign Part IV.

- Over $20,000: The IRS may require you to submit a copy of the signed appraisal with your return. Keep a high-resolution scan ready.

Important: the $5,000 threshold applies to similar items donated to the same charity within the same tax year. If you donate five paintings each worth $1,200 to the same museum in January and December, the aggregate is $6,000 and a qualified appraisal is required.

For tax year 2025 and 2026, the standard deduction stands at $16,100 for single filers and $32,200 for married couples filing jointly. If your total itemized deductions — including charitable gifts — do not exceed those amounts, you will not benefit from itemizing. Donors often bundle multiple years of donations into a single year or use a donor-advised fund to clear the threshold.

What Makes an Appraisal "Qualified" Under IRS Rules

Not every valuation document counts. The IRS definition of a qualified appraisal (Publication 561) includes specific requirements that go well beyond a dealer's verbal estimate or an auctioneer's insurance replacement figure.

A qualified appraisal must:

- Be prepared no earlier than 60 days before the donation date.

- Include a detailed description of the property (maker, date, size, medium, condition, and any identifying marks or signatures).

- State the fair market value and explain the valuation method used (comparable sales, income approach, or replacement cost).

- Include the appraiser's qualifications, signature, date, and a statement that they are a "qualified appraiser" as defined in IRC § 170(f)(11)(E).

- Disclose the appraisal fee — the fee cannot be contingent on the appraised value.

Who qualifies as a appraiser? The individual must hold a recognized appraisal designation (such as ASA, AAA, or ISA) with demonstrated expertise in the specific type of antique being valued. A generalist estate-sale operator or a dealer without formal appraisal credentials does not meet the IRS standard for items above $5,000.

For antiques specifically, the appraiser should reference comparable auction results, recent private sales of similar pieces, and published price guides. The more specific the comparables — same maker, period, condition tier — the stronger the appraisal stands if the IRS challenges it.

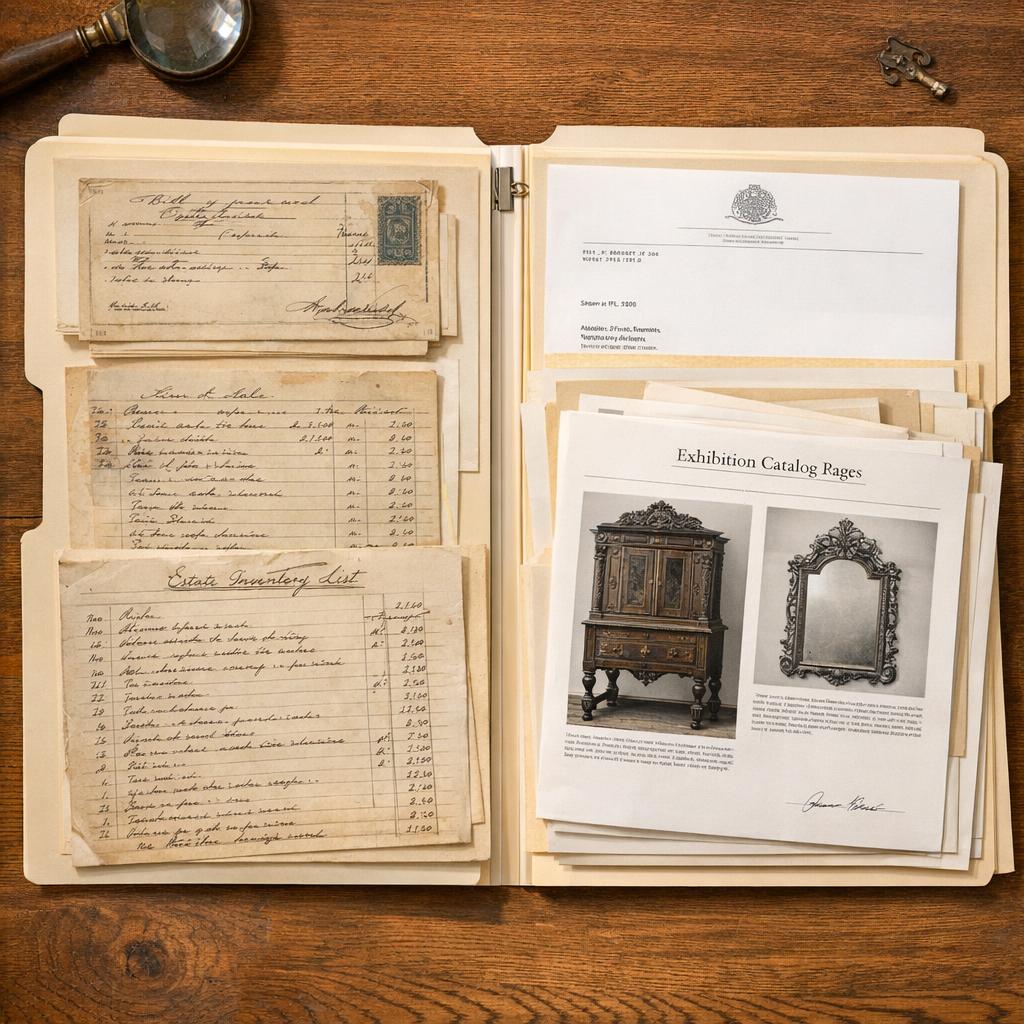

Your Pre-Appraisal Documentation Checklist

Before you even engage an appraiser, you should assemble a documentation file. A thorough file reduces the appraiser's research time (which lowers your fee) and produces a more defensible report. Think of it as building a provenance dossier that follows the object from creation to donation.

Here is what to gather for each antique:

| Document Type | What to Include | Why It Matters |

|---|---|---|

| Photographs | Full view, maker marks, condition issues, signatures/hallmarks | Primary evidence of identity and condition |

| Purchase receipt or bill of sale | Date, price, seller name, item description | Establishes acquisition date and cost basis |

| Provenance records | Previous owners, estate inventory listings, exhibition history | Strengthens attribution and supports higher valuation |

| Certificate of authenticity | Issuer name, date, specific claims made | Third-party confirmation of attribution |

| Restoration records | What was repaired, by whom, when, cost | Affects value — undisclosed restoration can undermine an appraisal |

| Previous appraisals | Date, appraiser name, value stated, purpose | Provides valuation history; useful for trend context |

| Auction catalog or sales record | Lot number, house, date, realized price | Comparable market evidence for similar items |

Items with a complete provenance file routinely appraise 20% to 50% higher than identical pieces with no documented history. A Chippendale secretary with a chain of ownership tracing back to the original family, plus photographs of the maker's brand and construction details, commands a very different valuation than the same form without any paperwork.

Free first look

Check tax-assignment fit before paying

Upload one clear photo for a preliminary scope check. This is not a qualified appraisal or tax advice; confirm the appraiser, report, timing, and Form 8283 fit in writing before purchasing.

Upload a photo for a free first lookFree. No card needed.

How to Photograph Antiques for Appraisal Documentation

Photographs are the IRS's first line of evidence. Publication 561 explicitly states that donors should support valuations with photographs. For antiques, the right images do more than show the object — they reveal maker marks, construction methods, and condition issues that drive value.

Follow this photography protocol for each piece:

- Overall front view: Place the piece against a neutral background. Shoot straight-on at eye level. Use natural, diffused light from one side.

- Back and underside: Many maker marks, inventory numbers, and construction clues appear on the back or bottom. Flip the piece and photograph these surfaces.

- Maker marks and signatures: Use macro mode or a close-up lens. Capture hallmarks on silver, furniture brands, potter's marks on ceramics, and any engraved or impressed signatures.

- Joinery and construction: For furniture, photograph dovetails, mortise-and-tenon joints, and screw types. Hand-cut dovetails signal pre-industrial manufacture; machine-cut dovetails indicate later production.

- Condition issues: Document cracks, repairs, replaced parts, finish loss, and insect damage. Do not hide flaws — an honest condition report strengthens the appraisal's credibility.

- Scale reference: Include a ruler or common object (a coin, a pen) in at least one shot so the appraiser can gauge dimensions from the photo.

Save all images at full resolution (at least 2 megapixels) and keep the originals unedited. You can add annotated copies with arrows or circles pointing to specific features, but the appraiser needs the clean originals too. Store the files in a dedicated folder named for each piece — e.g., Chippendale_Desk_1770/ — and include the folder in your appraisal packet.

Organizing Provenance and Ownership Records

Provenance is the documented history of ownership. For antiques, a strong provenance chain can multiply value — and it is equally critical for substantiating a charitable deduction. The IRS does not require provenance, but an appraiser cannot credibly value an item without it.

Key provenance documents, in order of importance:

- Original bill of sale or purchase receipt: The single most important document. It establishes when and where you acquired the piece and at what price.

- Estate inventory or probate listing: If you inherited the piece, the estate's inventory or probate filing that describes the item connects it to the original owner.

- Exhibition catalog or museum label: If the piece was displayed in a public exhibition, the catalog entry serves as third-party authentication.

- Previous appraisal reports: Even outdated appraisals show a valuation history and help the new appraiser understand trends.

- Dealer or auction house records: If you bought at auction, the catalog description and realized price for comparable lots provide market context.

Organize these documents chronologically in an archival folder or binder. Label each page with the item name and date. If the file is digital, scan everything at 300 dpi minimum and save as PDFs with descriptive filenames. A single, well-ordered provenance file is far more persuasive to an appraiser — and to the IRS — than a shoebox of loose papers.

What Happens After the Appraisal: Form 8283 Walkthrough

Once you have the qualified appraisal in hand, the next step is completing IRS Form 8283. This form is the bridge between your appraisal and your tax return. Missing or incorrect Form 8283 filings are among the most common reasons charitable deductions for antiques are disallowed.

Here is the sequence:

- Complete Part I: Describe each donated item (type, physical condition, approximate date of creation, and how you acquired it). State the fair market value and the method used to determine it.

- Complete Part II (if any item is $5,000+): This section requires the qualified appraisal. Include the appraiser's name, address, qualifications, and the date of the appraisal.

- Appraiser signs Part III: The appraiser must sign and date the form, affirming that the appraisal was prepared in accordance with IRS standards and that they are a qualified appraiser.

- Charity countersigns Part IV: The receiving organization must acknowledge receipt of the property by signing Part IV. This does not mean the charity agrees with the value — it confirms the item was received.

- Attach to your tax return: File Form 8283 with your Form 1040 for the tax year in which the donation was made. Keep a copy of the entire packet — appraisal, Form 8283, photos, and provenance — for your records.

Timing matters: the appraisal must be obtained no earlier than 60 days before the donation, and Form 8283 must be filed by the due date of your return (including extensions). If the deduction exceeds $5,000 and you fail to attach the qualified appraisal, the IRS can disallow the entire deduction — not just the portion above the threshold.

Common Mistakes That Trigger IRS Scrutiny

IRS enforcement of charitable deduction substantiation has intensified since 2024. The following errors are the most frequent reasons deductions for donated antiques are reduced or denied:

- Overvaluation without support: Claiming $50,000 for an antique with no comparables or a generic "insurance replacement" appraisal. The IRS compares your claimed value to actual auction results. A 200%+ overvaluation relative to market is a red flag.

- Missing photographs: Publication 561 specifically recommends photographs. An appraisal file with no images of the actual donated item is incomplete.

- Using an unqualified appraiser: A dealer's written estimate, an auctioneer's pre-sale guess, or an online valuation tool does not satisfy the qualified appraisal requirement for items above $5,000.

- Late or missing Form 8283: Filing the form after the return deadline, omitting the appraiser's signature, or failing to get the charity's acknowledgment — any of these gaps can disallow the deduction.

- Donating to a non-qualified organization: The recipient must be a 501(c)(3) organization or equivalent. Donating to a private foundation or a foreign charity may not qualify for the same deduction treatment.

If the IRS challenges your deduction, the burden of proof is on you. A complete documentation file — photos, provenance, qualified appraisal, and properly executed Form 8283 — is your best defense. Without it, the IRS can reduce the deduction to zero.

Record retention: keep your appraisal file and Form 8283 for at least three years from the date you file the return, or longer if the deduction was substantial. For items valued over $20,000, some advisors recommend retaining records for seven years or more.

When to Get a Second Opinion

Not every donation requires multiple appraisals, but there are situations where a second qualified opinion protects your interests:

- High-value single items: If one piece is appraised at $50,000 or more, a second independent appraisal adds credibility and reduces audit risk.

- Contested donations: If the charity or your tax advisor questions the valuation, a second opinion from a different credentialed appraiser can resolve the dispute.

- Insurance vs. fair market value divergence: Insurance replacement value is typically 150% to 200% of fair market value for antiques. If your insurance appraisal states $30,000 but the fair market value for donation purposes is closer to $15,000, understand the difference and document both figures.

- Complex collections: For estate collections with dozens of items spanning multiple categories (furniture, ceramics, textiles, metalwork), consider an appraiser who specializes in the dominant category and consult a second specialist for outlier pieces.

Current Market Context for Donated Antiques

The antique market has shifted significantly in recent years. While mass-produced Victorian furniture has softened, documented pieces with strong provenance and maker attribution continue to command premium prices at auction. A well-documented 18th-century American chair with a known maker can sell for multiples of an otherwise identical piece with no history.

Recent auction cycles in 2025 and early 2026 show that charity auctions featuring antique furniture and decorative arts with complete appraisal documentation consistently outperform those without. Donors who invest in thorough documentation before donating not only protect their tax deduction but also help the receiving charity present the item with confidence to future buyers or exhibition curators.

For donors considering a contribution to a museum, historical society, or university collection, the documentation file you prepare becomes part of the institution's permanent record for the object. Your diligence today becomes part of the piece's provenance chain tomorrow — potentially increasing its cultural and financial value for decades.

Get a qualified appraisal for your antique donation

Our credentialed appraisers specialize in antiques and decorative arts. Submit photos and provenance notes — we will route your item to the right specialist and deliver a written, IRS-ready appraisal.

- ASA, AAA, and ISA qualified appraisers

- Written reports compliant with IRS Publication 561

- Form 8283 ready for your tax return

Typical turnaround: 24–48 hours for initial assessment.

References and sources

- IRS Publication 561, Determining the Value of Donated Property — irs.gov/pub/irs-pdf/p561.pdf

- IRS Publication 526, Charitable Contributions — irs.gov/publications/p526

- IRS Form 8283 and Instructions, Noncash Charitable Contributions — irs.gov/forms-pubs/about-form-8283

- IRC § 170(f)(11)(E), Qualified Appraiser definition

- American Society of Appraisers (ASA), Personal Property Appraisal Standards — appraisers.org

- Nolo, When Are Appraisals Required for Donations? — nolo.com

Search variations collectors ask

Readers often search these questions — each is addressed in the guide above:

- What documents do I need for a charity donation appraisal?

- Does the IRS require a qualified appraisal for donated antiques?

- How to photograph antiques for an appraisal report?

- What is Form 8283 and when must I file it?

- How much does a qualified antique appraisal cost?

- Can I use an insurance appraisal for a tax deduction?

- What happens if the IRS audits my antique donation?

- How long should I keep donation appraisal records?

- Who qualifies as an IRS-approved appraiser for antiques?

- Do I need an appraisal for donations under $5,000?

Each question above is covered in detail in the valuation and documentation guide.