Most stock investors already understand the art market better than they think. They understand underpriced assets, growth bets, liquidity, and asymmetric risk. What changes is the evidence.

Art is not a stock. It is usually less liquid, harder to price, more expensive to transact, and more dependent on condition, provenance, taste, scholarship, and timing. A painting does not issue quarterly reports. A desk-and-bookcase does not publish earnings. A print does not trade on an exchange.

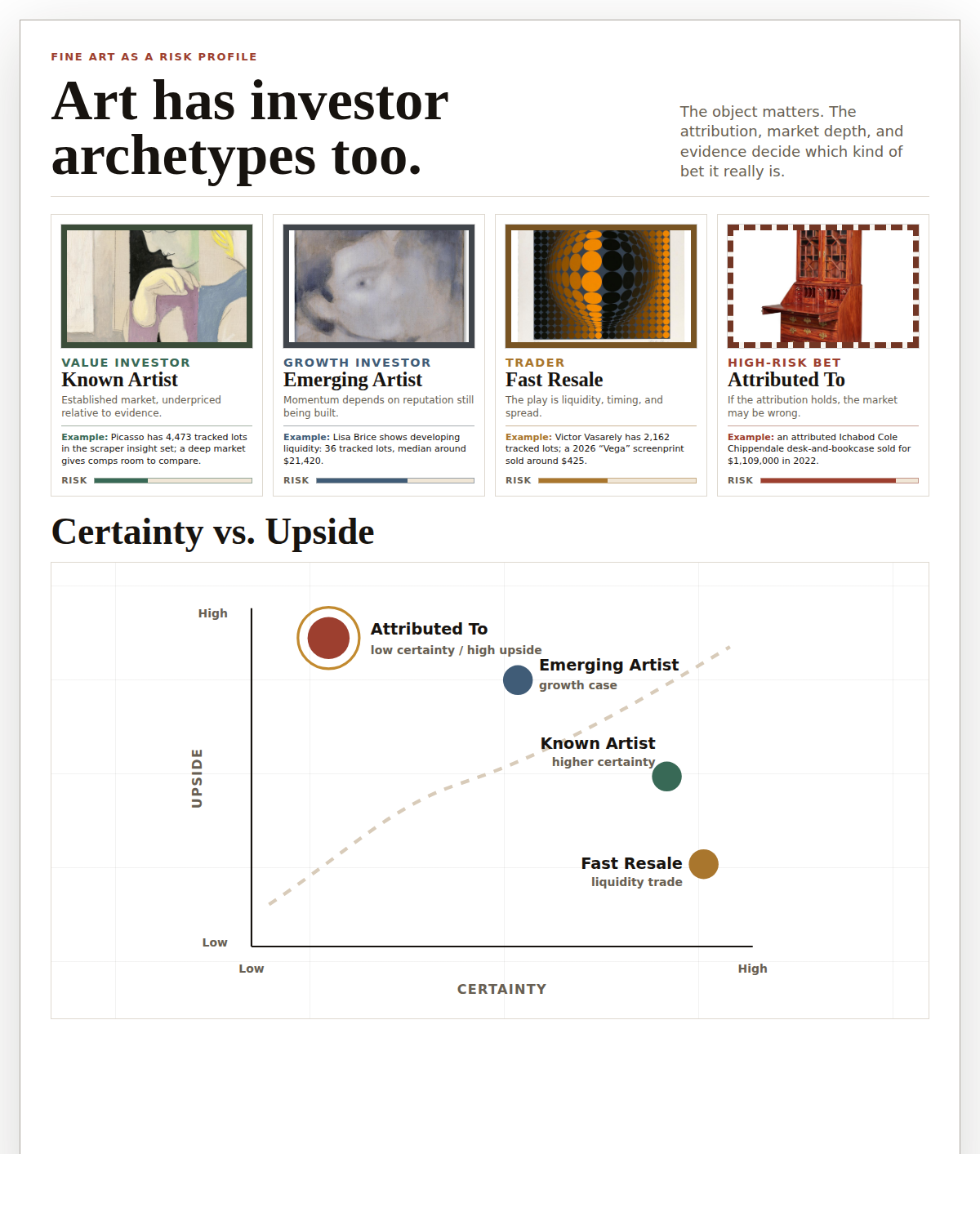

But many art purchases still have a recognizable risk profile. A buyer can look for established names with mispriced evidence. Another buyer can look for emerging reputation before the market fully catches up. A seller can focus on liquid objects that trade often. And a risk-seeking buyer can look at attribution language, where the gap between uncertainty and upside may be unusually wide.

The value investor: known artist, underpriced evidence

A value investor in art is usually not looking for a mystery. They are looking for a known artist where the evidence appears stronger than the current price, presentation, or market attention suggests.

That can happen when a work is poorly photographed, listed in the wrong category, described too weakly, offered in a quiet venue, or overlooked because the medium is less fashionable than the artist's headline market. The bet is not simply that the name is famous. The bet is that the evidence around the object supports a better reading than the market has priced.

The growth investor: emerging artist, developing market

The growth version is different. The buyer accepts that the auction record may still be thin. Instead of deep historical comparables, the case depends on reputation formation.

Signals might include gallery representation, institutional attention, critical writing, rising auction appearances, scarce strong works, and collector demand. The risk is not only whether the artist is talented. The risk is whether the market continues to care, and whether the specific work is the kind of example future buyers will want.

The trader: liquidity, timing, and spread

Some art behaves less like a long-term collecting thesis and more like a liquidity trade. Prints, editions, decorative works, and recognizable names at accessible price points can move more frequently than rare one-off objects.

The important question is not whether the object is glamorous. It is whether there is a broad enough buyer pool when it is time to sell. In that world, photography, platform, condition, edition details, framing, fees, and shipping can matter as much as taste.

The high-risk bet: attributed to

The most asymmetric art-market bet is often not the unknown artist. It is the almost-known one.

"Attributed to" does not mean authenticated. It usually means there is some evidence pointing toward an artist, maker, workshop, or school, but the authorship is not fully proven or universally accepted. That uncertainty is the risk. If the attribution weakens, the object can fall back toward follower, school, workshop, or decorative value. If the attribution strengthens, the market may have been materially underpricing the work.

The upside is not in the name alone. The upside is in the evidence improving.

Known artist

Established market, but the work may be underpriced relative to its evidence, condition, subject, or presentation.

Emerging artist

The market is still forming. Reputation, institutional attention, and scarcity matter more than long comparable history.

Fast resale

The focus is liquidity: how often similar objects trade, how many buyers exist, and whether the spread can survive fees.

Attributed to

The authorship is uncertain. The downside is real, but the upside can be large if stronger evidence changes the attribution case.

Real auction examples behind the analogy

These examples are not recommendations. They show how different kinds of art-market evidence can create different risk profiles.

The real balance sheet in art

In stocks, investors read balance sheets. In art, collectors read evidence trails.

| Investor question | Stock-market evidence | Art-market evidence |

|---|---|---|

| Is it underpriced? | Earnings, cash flow, assets, valuation multiples. | Comparable sales, condition, subject quality, provenance, artist period, and presentation. |

| Is growth still ahead? | Revenue growth, market share, guidance, adoption. | Gallery representation, institutional attention, auction frequency, critical writing, and collector demand. |

| Can I exit? | Volume, spreads, market depth. | Recent auction turnover, edition size, buyer pool, platform fit, fees, shipping, and condition risk. |

| What can change the price? | Earnings surprise, new information, sentiment shift. | New provenance, expert opinion, catalog inclusion, conservation findings, or changed attribution. |

What stock investors often miss about art

The biggest mistake is treating art as if price history alone is enough. In many cases, the object-level evidence matters more than the category. Two works by the same artist can have very different values because one has stronger provenance, better condition, a better subject, a more desirable date, or a cleaner authenticity case.

That is why art-market work feels slower than reading a price chart. The hard part is not only finding the past sale. The hard part is knowing whether that sale is actually comparable.

The discipline is familiar

Art is not a stock. But many art purchases still have a risk profile.

Known artist. Emerging artist. Liquid resale. Attributed work.

Different objects. Different evidence. Different risk. The discipline is familiar. The market just speaks another language.

Want the evidence read clearly?

For a painting, print, sculpture, or antique, the useful question is not only "what is it worth?" It is "what evidence supports that value?"

Start an appraisal Read about attribution language