Qualified Appraisal Checklist for Charitable Donations: appraisal and value basics

Qualified Appraisal Checklist for Charitable Donations research should start with identification, condition, provenance, and recent comparable sales. Use this guide to compare the signals that matter before paying for a formal appraisal or deciding whether to sell.

If your charitable gift is noncash and large enough to trigger IRS appraisal rules, the work is really about timing, independence, and paper trail discipline. The best checklist is the one that makes the appraiser’s conclusion easy to defend later: clear photographs, market evidence, a current report, and a clean Form 8283 trail.

This guide is written for donors, advisers, nonprofit teams, and estate planners who need a practical file they can use before the return goes out. It is not legal advice, but it does give you the same working checklist a qualified appraiser will expect to see.

Quick rule of thumb: when a gift is valuable enough to matter on a return, gather the evidence before filing and treat the appraisal as part of the gift packet, not an afterthought.

Two-step review

Share your qualified appraisal details with an expert

Share the basics and we’ll use them to prepare the right appraisal path, written quote, and next steps.

Please add the object details and an email address to continue.

Secure review. Clear next steps. Checkout only if you decide to proceed.

The qualified appraisal checklist

When you are collecting records for a charitable gift, keep the checklist narrow and practical. The goal is to show that the appraiser knew the object, knew the market, and wrote the report in time for the return.

-

Confirm the gift actually needs a qualified appraisal

Noncash gifts below the threshold can have different documentation rules, but once the value is high enough to matter, the file should be built with appraisal support in mind. That means identifying the property early, not after the return is nearly due.

- List the donor, the donee, and the date the charity received the property.

- Separate cash gifts from object gifts so the record stays clean.

- Keep a short memo explaining why the item is likely to require appraisal support.

-

Verify the appraiser is qualified for the object type

A qualified appraiser should be independent, experienced in the relevant market, and able to explain the conclusion in plain language. If the gift is a painting, jewelry lot, antique, or mixed estate parcel, the signer should show they actually work in that lane.

- Ask for category experience, recent comparable sales, and sample report language.

- Confirm there is no disqualifying financial interest in the gift.

- Look for a report that connects the object’s condition to the market result.

-

Order the appraisal early enough to stay inside the filing window

The report should be current enough to reflect the donation date and available before the tax return goes out. If the report is rushed at the end of filing season, there is less room to gather photos, title evidence, or a cleaner comparable set.

- Build in time for the appraiser to inspect the object or the best available photographs.

- Save drafts, emails, and notes so the timeline is clear.

- Do not wait for the charity acknowledgment before starting the appraisal.

-

Document the object like you expect someone to challenge the value

The strongest donation files read like a miniature case study. They include front-and-back images, signature or maker-marks, condition notes, measurements, provenance, and a short explanation of why the comparable sales are close enough to use.

- Photograph marks, labels, repairs, losses, and packaging if it matters.

- Keep provenance notes separate from the appraiser’s conclusion.

- Ask the appraiser to state whether condition or completeness changes FMV.

-

Complete Form 8283 cleanly and attach the right summary

The appraisal file and the tax form must agree. The object description, date of gift, appraised value, and signer details should match the report, and the donor should make sure the donee acknowledgment is in the packet before filing.

- Match the object description to the appraisal language.

- Keep the signed summary with the full report and backup photos.

- Double-check value fields before the return is submitted.

-

Store the file so it can survive an IRS review later

A qualified appraisal is not useful if the supporting records disappear. Save the report, the comps table, the donor acknowledgment, and any correspondence in one folder so the packet can be handed to an adviser or examiner without reconstruction work.

- Keep digital copies in a folder named for the donor and the tax year.

- Retain the appraiser’s contact details and scope of work.

- Note any later repairs, supplemental images, or corrected descriptions.

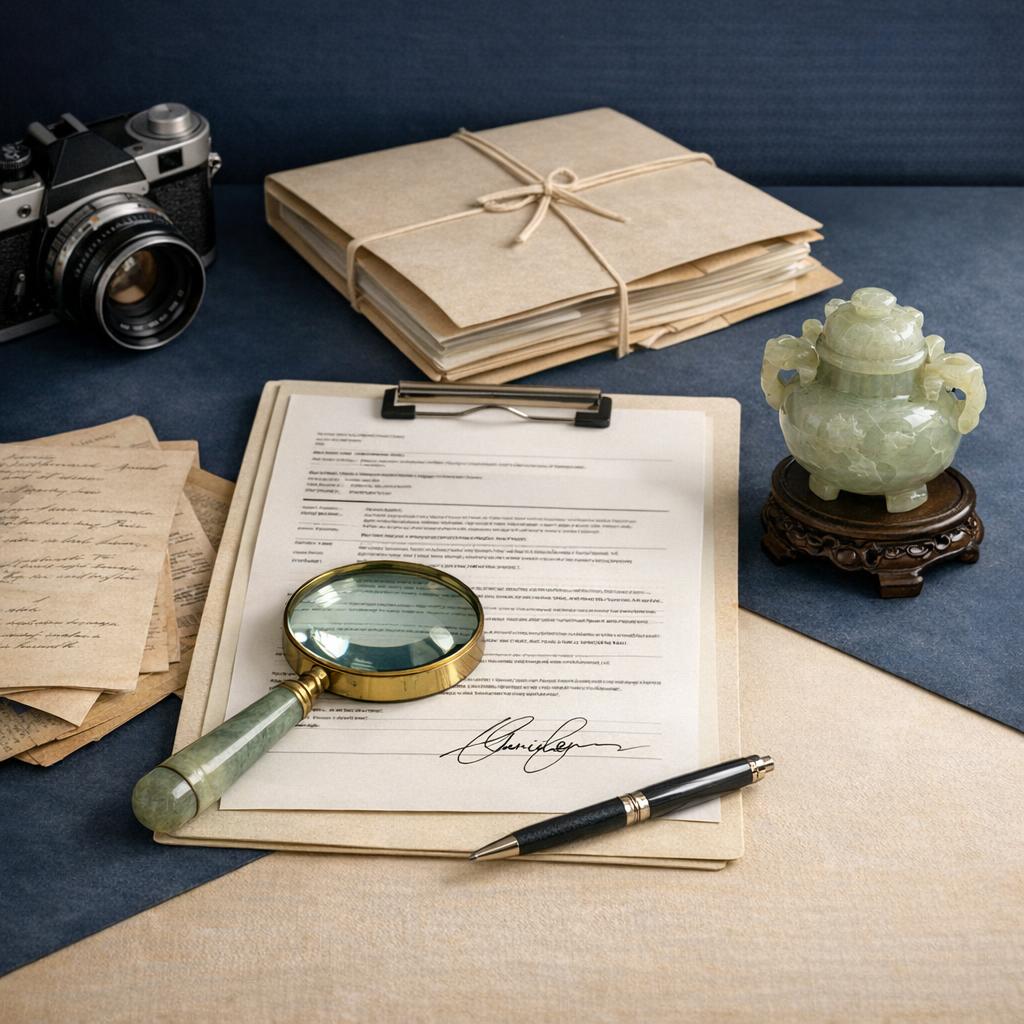

Visual guide: the file at a glance

These images are deliberately single-subject and documentary in tone. They reinforce the same message as the checklist: date the gift, confirm the signer, keep the evidence, and make the market path easy to follow.

Frequently asked questions

Do I always need a qualified appraisal for a charitable donation?

No. Smaller noncash gifts can fall under different documentation rules. The practical checkpoint is whether the gift is large enough that the IRS expects formal appraisal support and a clean Form 8283 trail.

How close to the gift date should the appraisal be?

The safest approach is to order it early enough that the report still reflects the donation date and lands before the return is filed. If the appraisal is being written at the last minute, the file is probably too tight.

Can the charity or donor sign the appraisal?

The signer should be an independent qualified appraiser, not the donor and not someone with a disqualifying interest in the gift. Independence matters because the report needs to hold up after the donation has already happened.

What belongs in the documentation packet?

Keep the report, the comp summary, front-and-back photos, provenance notes, the charity acknowledgment, and the completed Form 8283 together. If you can hand the whole packet to an adviser without explanation, you are close to done.

References and notes

- IRS Publication 561: Determining the Value of Donated Property

- IRS: About Form 8283, Noncash Charitable Contributions

- Appraisily editorial policy and sourcing standards

- All comp examples in this article were drawn from Appraisily auction data to show how a market trail is documented, not to provide tax advice.

Long-tail search variations

- What is a qualified appraisal for charitable donations? Useful when you are checking the basic IRS rule set.

- When do I need Form 8283 for a noncash gift? Usually the first question once the donation gets large enough to matter.

- How recent should a charitable donation appraisal be? Timing is the difference between a usable report and a stale one.

- Who can sign a qualified appraisal for the IRS? The signer should be independent and knowledgeable in the object category.

- What records should I keep with a donation appraisal? Photos, provenance, comps, acknowledgments, and the appraisal itself.

- Can art and jewelry use the same appraisal checklist? The paperwork is similar even when the market evidence is different.

- What happens if the charity does not sign Form 8283? It is a warning sign that the file needs more attention before filing.

- How do I prove fair market value for a donation? Use recent comparable sales and explain why they match the gift.

How We Research Valuation Data

Our appraisal guides are based on auction results, dealer pricing data, and professional appraiser insights. We may earn a commission when you use our free professional appraisal service. Learn about our editorial standards.

Choose your next step

Use the path that matches the decision you need to make about the item.

Not sure it is worth appraising?

Start with a lower-friction screen to understand the likely category, evidence, and next step.

Upload photos for a free first lookWant proof before paying?

See how a signed report documents photos, comparable evidence, condition notes, and value conclusions.

View signed report sampleNeed a signed report?

Use this for insurance, estate, donation, resale, or documented value decisions.

Need documentation now? Start signed appraisalNeed local or specialist help?

Compare directory options when the work needs in-person review or a specialist near you.

Find local specialistsSee what the report looks like

Sample reports show how photos, comparable evidence, condition notes, and a value conclusion are documented.

Qualified appraisal service

Need a defensible appraisal before you file the return?

If the gift is valuable, mixed, or close to the filing deadline, start with a clean appraisal packet and a specialist who can explain the fair market value in writing.

- Review photos, provenance, and valuation timing.

- Compare the market evidence against your donation file.

- Move into the start flow with a clear next step.

Best for art, jewelry, antiques, and mixed estate gifts that need a clean support file.